Online vs Land-Based Gambling: How British Spending Habits are Shifting

The UK’s high streets are witnessing a silent revolution as gambling pounds migrate from betting shops to digital screens. This fundamental shift in consumer behaviour is reshaping the landscape of UK gambling retail, with profound implications for local economies, employment, and community spaces. Driven by technology and accelerated by recent global events, this transition from physical to digital is a core focus of contemporary UK economic research, offering critical insights into the future of retail forecast Britain.

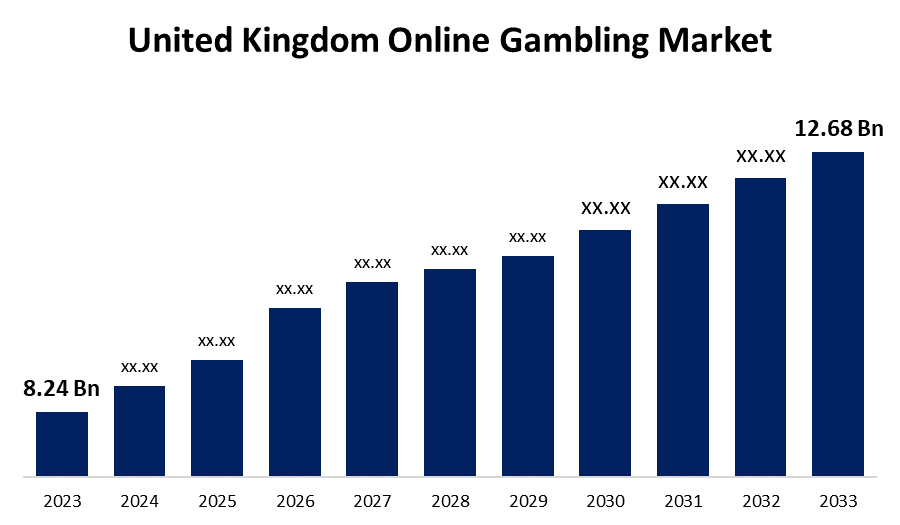

The Digital Surge: Online Gambling’s Dominance

The data underscores a decisive tilt towards digital platforms. According to the latest figures, online gambling now accounts for over 60% of the UK’s remote gambling yield, with market leaders like Bet365 and Paddy Power defining the new frontier. This digital dominance is not just a segment of the market; it is becoming the market itself, fundamentally altering revenue streams and consumer engagement models across the nation. The convenience of placing a bet from one’s sofa has proven to be a powerful draw, catalysing a sustained period of growth for the online sector that shows little sign of abating.

Mobile Betting Boom

The catalyst for this surge is unequivocally the smartphone. The proliferation of dedicated, user-friendly mobile apps has driven a staggering 25% year-on-year increase in online betting activity. For many consumers, the betting shop is now in their pocket, accessible 24/7. This constant availability has fragmented gambling sessions into smaller, more frequent interactions throughout the day, a pattern that physical locations simply cannot accommodate. Bet365, the UK’s largest online gambling company by revenue, has built its empire largely on the back of its intuitive and comprehensive mobile platform, setting the standard for the industry.

Live Casino and In-Play Trends

Beyond simple sports betting, online platforms have successfully replicated—and arguably enhanced—the thrill of live action. Live dealer casinos and sophisticated in-play betting markets have bridged the gap between the digital and the tangible. Players can now stream real-time roulette wheels or blackjack tables hosted by human croupiers, while simultaneously betting on dynamic odds in a football match. This fusion of real-time footage, instant data, and immediate wagering creates an immersive experience that is drawing traditional casino and sports betting patrons online.

High Street Retreat: The Decline of Physical Bookmakers

As digital channels thrive, the traditional bookmaker high street is contracting. Iconic brands like William Hill and Ladbrokes have been forced to shutter hundreds of shops, reflecting a stark 15% drop in high street betting outlets since 2019. This retreat is more than a business adjustment; it represents a significant change in the social and commercial fabric of many town centres, particularly in less affluent areas where these shops were once community fixtures.

Shop Closures and Job Losses

The scale of the retreat is concrete and impactful. William Hill closed 119 betting shops in 2023 alone, a move emblematic of the wider industry’s strategic pivot towards online operations. Each closure represents not just a vacant retail unit but also local job losses and reduced footfall for neighbouring businesses. The cumulative effect across the UK has been a substantial reduction in retail employment within the gambling sector, shifting economic activity from local high streets to corporate digital hubs often located elsewhere.

The Role of Fixed Odds Betting Terminals

This decline was significantly accelerated by the 2019 regulatory crackdown on Fixed Odds Betting Terminals (FOBTs). The government’s decision to slash the maximum stake from £100 to £2 severely impacted the revenue model of physical betting shops, which relied heavily on these high-speed electronic machines. For many operators, the new regulation rendered a large portion of their estate economically unviable, forcing a rapid consolidation of their physical presence and hastening the transition to online platforms where such stake limits do not apply with the same rigidity.

Driving Forces: Why Brits are Choosing Online

Understanding this shift requires examining the compelling advantages online platforms hold. The migration is not incidental; it is a rational consumer response to a superior value proposition centred on convenience, cost, and innovation.

Convenience and Accessibility

The primary driver is undeniable convenience. The ability to gamble anytime, anywhere, without the need to travel to a specific location, aligns perfectly with modern, time-poor lifestyles. This was dramatically amplified during the COVID-19 pandemic, when lockdowns forced the closure of all land-based venues, accelerating digital adoption by several years in a matter of months. For many, the habit formed during this period has persisted.

Bonuses and Promotions

Online operators aggressively compete for market share using financial incentives that physical shops cannot feasibly match. New customers are enticed with significant sign-up bonuses, free bets, and enhanced odds. The competitive digital landscape means these promotions are constant, creating a powerful economic pull factor. Consider the typical online welcome offer compared to a high street shop:

- Online: “Bet £10, Get £30 in Free Bets” plus ongoing price boosts and loyalty points.

- High Street: Perhaps a free bet slip with a new account, but rarely matching the scale of digital bonuses.

Economic Ripple Effects: From Casinos to Communities

The economic impact of this transition is multifaceted, creating winners and losers across different sectors and geographies. While online operators report record yields—UK Gambling Commission data shows online gambling yield reached £5.7 billion in 2023—the story on the ground is more complex.

Casino Economic Impact

Large land-based casinos are navigating this shift by evolving into experiential destinations. The Hippodrome Casino in Leicester Square is a prime example, contributing over £30 million annually to the London economy not just through gambling, but via its restaurants, bars, and live theatre shows. It has become a night out, not just a betting destination. In contrast, regional cities like Manchester have felt the sting of casino closures, which remove not only jobs but also nighttime economy anchors that support hospitality and taxi services.

High Street Vacancies and Regeneration

The closure of betting shops contributes to the growing challenge of high street vacancies. These often-small units can be difficult to repurpose, leading to stretches of boarded-up shops that deter investment and reduce area attractiveness. The future of these spaces is a key question for urban planners. Some communities are seeing these units converted into local service hubs, independent retail spaces, or cafes, as part of wider high street regeneration efforts aimed at creating more diverse and sustainable town centres.

Future Forecast: Where is UK Gambling Heading?

Based on current trajectories and ongoing UK economic research, the retail forecast Britain for gambling points towards a hybrid future, albeit one with a distinctly digital centre of gravity.

Regulatory Changes

The impending overhaul of the Gambling Act will be the single biggest factor shaping the market. Expected measures include stricter affordability checks, tighter controls on online stakes and bonuses, and potentially a mandatory levy on operators to fund treatment and research. These regulations will likely increase operational costs for online firms but could also level the playing field slightly by mitigating some of their aggressive promotional advantages.

Hybrid Models Emerge

We predict a continued rise in online spending, but land-based venues will survive by doubling down on experiences that cannot be replicated digitally. Grosvenor Casinos’ refurbishments, focusing on premium dining and entertainment, exemplify this trend. The future lies in hybrid models: online platforms for day-to-day betting, and physical venues for social nights out, major sporting event viewings, and premium gaming experiences. Brands like Entain (owner of Ladbrokes and Coral) are actively integrating their online and offline offerings to capture both revenue streams.

In conclusion, while the momentum behind online gambling appears unstoppable, a balanced and sustainable retail forecast for Britain requires supportive policies that acknowledge the value of land-based venues. The goal should not be to halt digital progress, but to foster an environment where high streets can adapt, innovate, and find new purposes, ensuring the economic impact of this shift ultimately benefits a broader spectrum of UK communities.